Working From Home Deductions - Shortcut Method vs Fixed Rate Method

The Australian Taxation Office has announced a temporary method for claiming deductions for working from home. It will allow people to claim 80 cents per hour for all their running expenses, rather than calculating costs for specific running expenses.

Taxpayers will have the choice between the new shortcut method and the old fixed rate method, known as the 52 cents method. This allows them to choose between simplicity and less record keeping, or choosing to prepare and keep records and possibly claim bigger tax deductions.

SHORTCUT METHOD

The shortcut method will allow taxpayers to claim 80 cents for each hour worked from home and covers all deductible running expenses. These running expenses include:

- expenses related to heating, cooling and lighting in the area you are working from

- phone and internet expenses

- cleaning costs for a dedicated work area

- computer consumables and stationary

- depreciation of home office furniture, furnishings and equipment

Under this method, separate claims cannot be made for any of the above running expenses.

Using the shortcut method could result in a claim for running expenses being lower than a claim under existing arrangements (including the existing 52 cents per hour method for certain running expenses).

This method will only apply for the hours worked at home between 1 March 2020 and 30 June 2020. After this period the ATO will review the arrangement for the next financial year as the COVID-19 situation progresses. Hours outside of this period will be calculated using the fixed rate method.

If taxpayers opt to use the shortcut method, they are only required to keep records showing the hours they have spent working from home. This could be done through timesheets, rosters, a diary or similar document that sets out the hours worked.

Where there are multiple people living in the same house, each can claim this new rate. For example, a couple living together could each individually claim the 80 cents per hour rate. The requirement to have a dedicated work from home area has also been removed.

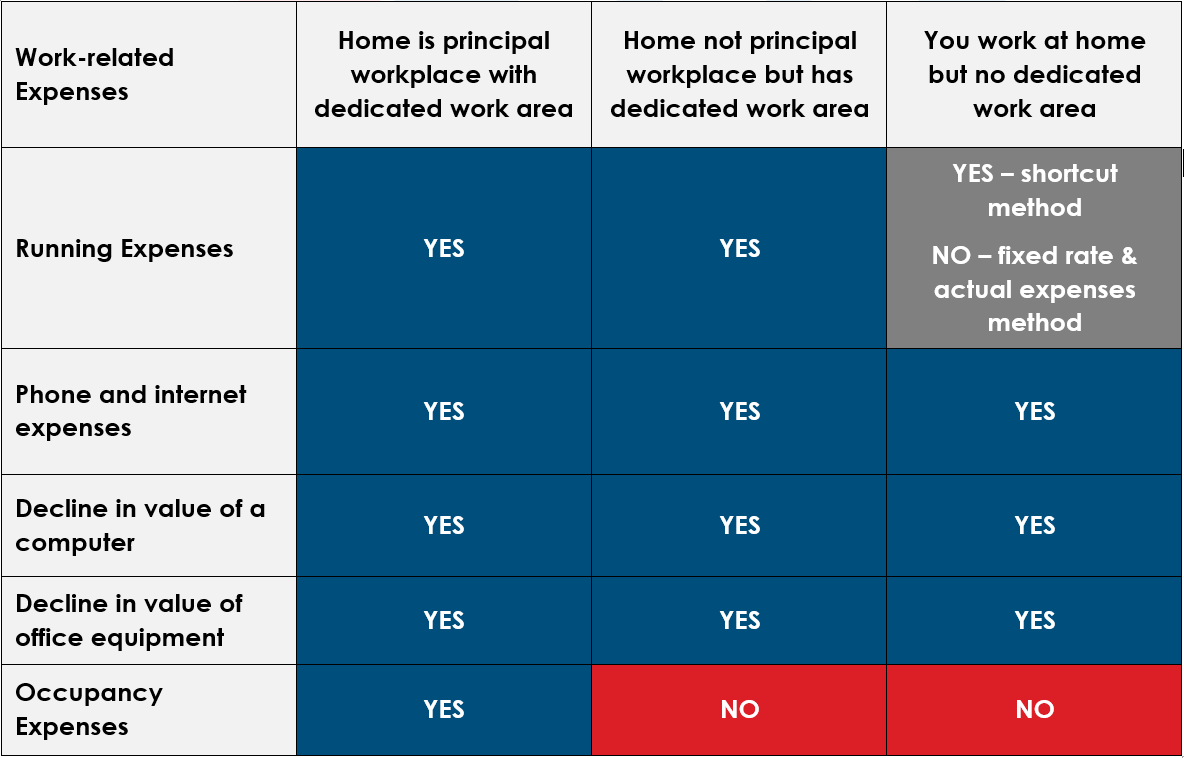

Occupancy expenses such as rent, mortgage interest, property insurance and land taxes will not become deductible due to circumstances caused by COVID-19.

FIXED RATE METHOD

The fixed rate method will allow taxpayers to claim running expenses such as heating, cooling, lighting, cleaning and the decline in value of furniture at 52 cents for every hour worked from home.

Under this method taxpayers need to separately calculate the work-related portion of items such as phone and internet expenses, computer consumables, stationery and the decline in value of a computer, laptop or similar device.

When calculating phone and internet costs, if the taxpayer is claiming up to $50 in total, they may make a claim based on the following, without having to analyse their bills:

- $0.25 for work calls made from your landline

- $0.75 for work calls made from your mobile

- $0.10 for text messages sent from your mobile

Taxpayers will need to allocate their use between personal and work-related, and they must do so on "a reasonable basis". If choosing to use the fixed rate method, taxpayers must keep records such as:

- a diary for a representative four-week period to show usual pattern of working at home

- receipts or other written evidence, including for depreciating assets purchased

- diary entries to record small expenses ($10 or less) totalling no more than $200, or expenses taxpayers cannot get any kind of evidence for

- itemised phone accounts to identify work-related calls, or other records, such as diary entries.

HOME OFFICE EXPENSES YOU CAN AND CAN'T CLAIM

ACTUAL EXPENSES METHOD

If a taxpayer has a dedicated work area, they can claim further running costs and the decline in value of office furniture used in the area for work purposes. To claim taxpayers can:

- record the number of actual hours they worked from home during the income year

- work out the cost of their cleaning expenses by adding together their receipts and multiply it by the floor area of your dedicated work area

- work out the cost of their heating, cooling and lighting by working out the following:

o the cost per unit of power used (using their utility bill)

o the average units used per hour – this is the power consumption per kilowatt hour for each appliance, equipment or light used

o the total hours used for work-related purposes while working at home.

Taxpayers must also take into account the use of this area by other members of their household, if applicable, and apportion their expenses accordingly.

- To calculate the deduction for the decline in value of equipment, furniture and furnishings that cost more than $300, the item must be depreciated and apportioned to reflect work-related use.

Where the taxpayer has a phone or internet plan they can claim actual phone and internet expenses by determining the percentage of work use over a four-week representative period, which can then be applied to the full year. The taxpayer needs to work out the percentage using a reasonable basis. This could include:

- the number of work calls made as a percentage of total calls

- the amount of time spent on work calls as a percentage of total calls

- the amount of data downloaded for work purposes as a percentage of total downloads.

- If the taxpayer has a bundled plan, they need to:

o apportion the cost of the plan between the services provided, and

o identify the work use for each service over a four-week representative period during the income year, which can then be applied to the whole year

If you would like to discuss this please contact our office.